Sorry, but your login has failed. Please recheck your login information and resubmit. If your subscription has expired, renew here.

They’re the best of the best—carriers with the vision to anticipate where the trucking market is heading and the operational discipline to deliver day in and day out.

They’re growing alongside America’s $1 trillion trucking network, investing in people, equipment and technology while maintaining the service levels that shippers demand. Many boast on-time performance rates approaching 99%—numbers they’ll proudly document if you ask.

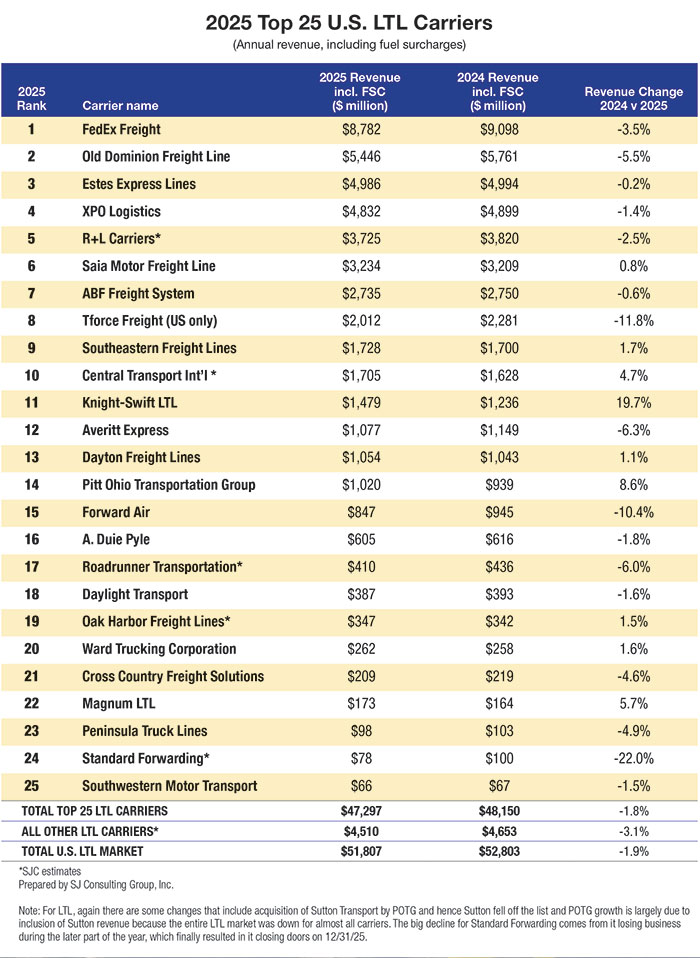

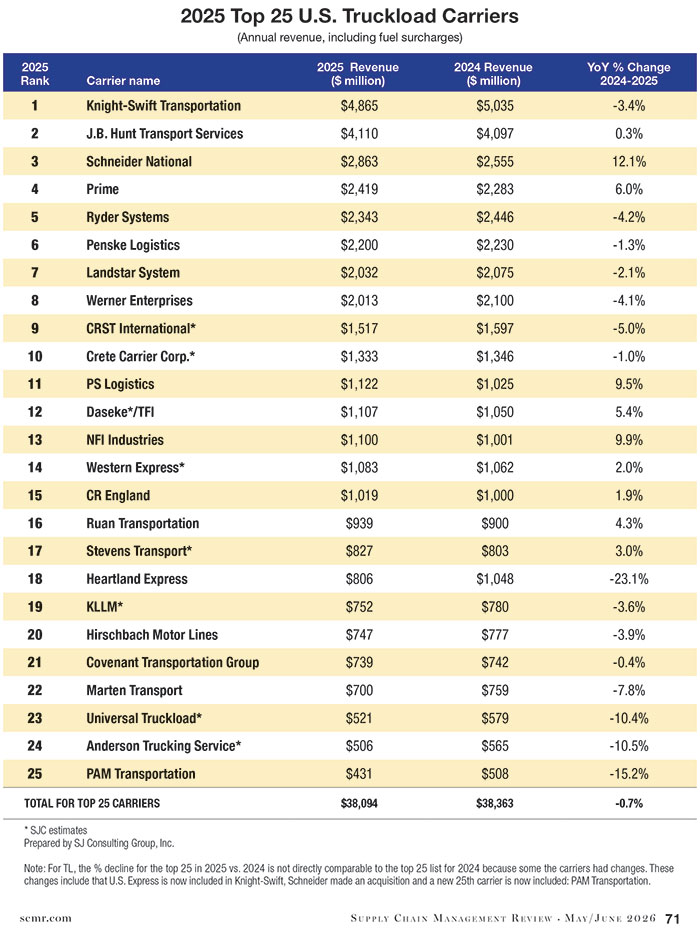

They’re the 50 largest and most influential trucking companies in the country: 25 operating in the highly fragmented, roughly $400 billion truckload sector, and 25 competing in the smaller but equally vital $58 billion less-than-truckload (LTL) market. They’re the Top 50.

SC

MR

Sorry, but your login has failed. Please recheck your login information and resubmit. If your subscription has expired, renew here.

They’re the best of the best—carriers with the vision to anticipate where the trucking market is heading and the operational discipline to deliver day in and day out.

They’re growing alongside America’s $1 trillion trucking network, investing in people, equipment and technology while maintaining the service levels that shippers demand. Many boast on-time performance rates approaching 99%—numbers they’ll proudly document if you ask.

They’re the 50 largest and most influential trucking companies in the country: 25 operating in the highly fragmented, roughly $400 billion truckload sector, and 25 competing in the smaller but equally vital $58 billion less-than-truckload (LTL) market.

They’re the Top 50. And as they’ve done for the past 23 years, our research partners SJ Consulting and Ship Matrix rank these carriers by size—but the list reflects far more than revenue alone.

It highlights the strategies, operational excellence and leadership that allow these companies to thrive in one of the most competitive industries in the U.S. economy.

Which raises the central question: What really makes a great trucking company? Is it long-term strategy? Vision? Day-to-day execution? Or the culture that drives employees to buy into that vision and deliver for customers every day?

What sets them apart?

We asked several top executives to candidly discuss what makes a great trucking company truly great. Their answers touched on everything from long-term vision to the day-to-day operational execution required to deliver on that vision.

“Strategy is what drives everything we do,” says Pitt Ohio president Chuck Hammel. “Our strategy is where we develop and nurture our culture and our service offerings. Our culture is the foundation of who we are as a company—and why we have succeeded for so long.”

“We firmly believe our culture has been—and continues to be—the single greatest contributor to our company’s performance and long-term success,” says Kent Williams, executive vice president of sales and marketing for Averitt Express, which operates a diversified trucking network. “It’s truly our secret sauce and is central to how we operate every day.”

Williams notes that 22% of Averitt’s employees, across all job classifications, have been with the company for more than 20 years. “We believe that speaks directly to the strength of our culture and the value we place on our people,” he adds.

Experienced trucking executives, well aware that the industry is a derived-demand business, have been waiting the better part of three years for freight demand to rebound. In 2026, they’re still waiting.

Asked to describe the overall domestic economy in 2026, Hammel summed it up in a single word: “Uncertainty.” Then, after a pause, he added: “Well, when has anything ever been certain

in this industry?”

Averitt’s Williams says the greatest short-term threat remains the broader economic environment, which has only recently begun to show modest signs of improvement. Longer term, he points to disruptive forces such as autonomous vehicles, emerging technologies and shifting market dynamics.

“We address these uncertainties by relying on the strength of our people and maintaining an innovative, flexible mindset,” Williams says. “By staying open to change and acting quickly when conditions shift, we’re able to adapt and continue delivering value to our customers.”

Next, we take our annual deeper dive into how some of the leading carriers in our Top 50 are navigating today’s market challenges.

Leading on pricing

Trucking rates have been in the doldrums for the past three years. After the pandemic, there was a modest rebound in 2022, but the long-awaited surge in rates has yet to materialize—despite scores of bankruptcies among small and midsize fleets.

Veteran trucking executives say they’ve seen this cycle before.

“The introduction of real price competition forever changed our industry and the makeup of the carriers,” says Peter Latta, chairman and CEO of A. Duie Pyle, one of the Northeast’s most prominent LTL carriers.

“If all you look at is the number on the freight bill, we may appear a little more expensive,” says Greg Plemmons, executive vice president and COO of Old Dominion Freight Line (ODFL), the nation’s second-largest LTL company. “But factor in our on-time service, lack of claims for damage and all the other costs involved, and our customers feel like they’re getting great value from us—and they are.”

“There’s more price discipline,” says Geoff Muessig, chief marketing officer at Pitt Ohio, another strong LTL carrier in the Northeast. Asked why, he adds: “It’s not because trucking executives are any smarter. It’s because all our customers use the same costing models.”

While decades of trucking rate wars have taken their financial toll, Pyle’s Latta says the survivors have learned the hard way that competing solely on price is rarely a winning strategy.

“Today, most of the remaining players appear financially sound as the market has largely reached equilibrium,” he says. “But I hope the surviving carriers have vicariously learned the lessons—and the consequences—of irrational and undisciplined pricing.”

Averitt’s operations include roughly 3,500 trailers and span high-volume regional LTL service as well as dedicated truckload operations. Executives say that diversified structure helps retain customers as their transportation needs evolve.

“Our diversification across five service lines is a critical driver of our performance,” adds Averitt’s Williams. “This structure allows us to deliver best-in-class service and tailored solutions across multiple segments while remaining flexible and resilient in a changing market.”

The ODFL factor

No single carrier dominates its space quite the way Old Dominion Freight Line does. A perennial leader in our Top 50 rankings, ODFL’s position is no accident. The carrier plans aggressively for future demand—looking not only at freight levels this summer, but at where the market could be heading by 2030.

Adam Satterfield, ODFL’s executive vice president, assistant secretary and CFO, said recently on an earnings call that the company’s internal target is “generally to have 20% to 25% excess capacity.” ODFL did not open any new service centers last year.

Satterfield acknowledged that while capacity may not be top of mind for many carriers right now, that can change quickly.

“While capacity isn’t maybe on everybody’s mind right now, it hasn’t been that long ago when we’ve seen periods where the environment does turn—and when it turns, it generally turns very quickly in our industry,” he said.

And when that happens, ODFL expects customers’ focus to shift quickly back to which carriers have available capacity—not only in service centers, but also in labor, equipment and the ability to respond to rising demand.

“That’s a big part of our value proposition and why we feel like we’re better positioned than anyone to respond when the market eventually turns positive,” Satterfield adds.

ODFL exceeded expectations in the fourth quarter of 2025, the most recent full quarter available, and struck a generally bullish tone about demand heading into 2026. January trends reflected below-average seasonality, due in part to weather. Analysts expect ODFL’s first six months to fall slightly below earlier projections.

ODFL’s fourth-quarter operating ratio (OR) came in at 86.7, slightly above management’s conservative estimate. Fourth-quarter tonnage declined 10.7%, but remained within normal seasonal

patterns. January revenue per day fell 6.8%, with tonnage down 9.6% per day—suggesting another soft start to 2026.

Of course, rival LTL carriers are hardly conceding any ground to ODFL.

“I believe our operations group is second to none,” says Pitt Ohio’s Hammel. “We run, on average, more than 500 bills through each terminal with an on-time next-day service record of over 97%. I think our consistent service through the years sets us apart in the industry.”

Looking ahead with AI

Artificial intelligence means different things to different people across industries.

For a technology giant like Amazon, AI investment is measured in the hundreds of billions. The company recently said it plans nearly a 60% increase in AI spending—roughly $200 billion this year compared with $128 billion last year—far above Wall Street projections.

For trucking companies, those kinds of investments are simply not realistic. Most industry executives instead focus on the practical ways AI might gradually reshape operations.

“Near term, the biggest challenge I see is how to integrate AI not only into our processes, but also to answer the broader question of how it will change the way we do business,” says Pitt Ohio president Chuck Hammel. “The LTL industry still relies heavily on paper and phone calls. Our challenge is figuring out how to eliminate both while continuing to deliver exceptional customer service.”

Technology innovation has long been a focus at Pitt Ohio. The carrier was one of the first major trucking companies to compile detailed customer-by-customer data on every piece of freight moving through its network.

Unlike many carriers, Pitt Ohio uses that data to build precise pricing models based on the actual cost of moving freight through its network. The company moved away from traditional general rate increases (GRIs) years ago, instead relying on customer-specific data to justify individual rate adjustments that cover costs while preserving modest profit margins. Other large LTL and truckload carriers have gradually followed similar approaches, although GRIs remain common across the industry.

“We’ve been innovators in this industry since our early days,” adds Hammel. “It’s simply part of our DNA.”

SC

MR

More Trucking Market

Explore

Explore

Topics

Business Management News

- Innovators Netstock, Pickle Robot win NextGen Solution Provider awards

- Bigger trucks versus broken bridges and roads

- From salon to dock door: Repurposing scheduling software for inbound flow

- The biggest barrier to AI in supply chains isn’t technology

- Rebuilding a planning function around the physical world

- Why companies blame the wrong supplier … and miss the real failure

- More Business Management

Latest Business Management Resources

About the Author

John D. Schulz, Contributing Editor, SCMR

John D. Schulz has been a transportation journalist for more than 20 years, specializing in the trucking industry. John is on a first-name basis with scores of top-level trucking executives who are able to give shippers their latest insights on the industry on a regular basis.

Follow SCMR on social media.

@SupplyChainManagementReview on Facebook

@SCMR on Twitter

SCMR on Linkedin

Subscribe

Supply Chain Management Review delivers the best industry content.

Editors’ Picks